Investing for your Child

Investing for your Child

How to successfully invest in The Stock Market for your minor child

INVESTING FOR MINORS

First off congrats to anyone who has made a decision to invest with or for your child. Regardless of their age, every child should have an investment account that’s built for the the long term being that they’re young. Please keep in mind, and take into consideration I am not a professional financial expert, I am simply someone trying to help and point you in the right direction so please seek out a professional or tax consultant if you have any questions beyond the basic scope of information. The intention of this news letter is to provide basic information to help you invest for yourself and child. With that said, let’s hop right into the thick of things. The benefits of investing early for a child improves their ability and chances of not having money concerns later in life. It also teaches them patience, and the importance of saving money for retirement or life early. Think about the impact this may have had on your life, lack of money or income. The one thing minors have that adults don’t have is more time, time is the greatest factor in investing. Someone who starts investing at 10 has more time to invest and build compound intrest than someone 80. So time, is a huge plus for investing early. Before we begin, please share this and give it a like it helps me along with the algorithms on Substack

So how exactly do I invest for my child?

It’s very simple, but to start you will need name, basic information, might even need your child social security number, if you don’t have it, you still may be able to move forward but clarify that information

There are various accounts such as Brokerage accounts, IRA, IRA Roth, and others but the ones specifically for children or minors are UGMA & UTMA

UGMAs and UTMAs are custodial accounts with assets owned by the minor. Contributions (gifts or transfers) into UGMAs and UTMAs cannot be revoked, and the minor beneficiary cannot be changed. Once the minor reaches adulthood (which depends on the law of the state that governs the UGMA or UTMA), the custodian must turn over all the assets remaining in the account to the former minor. So what this means is that once the child reaches a certain age you have to give the account and assets to them. For example, let’s say you start when your child 2 years old, when they’re 18 depending on your state rules, and regulations you may have to hand over the account to them

Any adult family member, court-appointed guardian, or organization can agree to act as custodian of the account. The custodian must reside in the United States or a U.S. territory and be either a U.S. citizen or resident alien.

This above just means anyone can act on behalf of the child but you must be an American.

A custodian may designate a successor custodian or name a limited agent to act on their behalf.

You can choose someone to take over the account you created, let’s say a trusted aunt or uncle in the event you perish, or can’t act on behalf of the account for your child

There could be a significant impact on federal financial aid for college as assets in the account are owned by the minor.

This just means that you should consult a financial or tax consultant before you hand over the account, but in my opinion this money can be used towards college, and has more flexibility than a traditional 529 account used for college savings

What’s the differences in UTMA & UGMA?

The UTMA, which started in 1996, allows more assets including physical assets, such as real estate, art, and cars. Another key difference is the age your child gets custody of the funds. The UGMA automatically transfers to your child's custody when they turn 18 years old. For the majority of you, UGMA will be the one you want to select. Write that down, the UGMA account

Another key difference is the age your child gets custody of the funds. The UGMA automatically transfers to your child's custody when they turn 18 years old. The UTMA offers more options. In many states, you can choose an age between 18 and 25, which may help parents of children who aren't mature enough to receive a large sum of money if not going to college. So this is basically saying it’s age differences between the two but to decide what’s best for you, that’s a personal decision but UGMA is what the majority go with. It can become confusing choosing between UGMA, UTMA, and College 529 Savings Plans because they all save for the future of your child. There are major differences…..so make sure you understand the differences. Oh and Google is your best friend

What are the Pros of starting a UGMA?

Your child can use the funds for any purpose, not just college. Not every child goes to college or want to go to college so it’s flexibility

Creditors can't come after the assets.

Anyone can open a UGMA or UTMA account, there aren't any income limitations. So that means anyone can do it even if you make a lot

A wider selection of investment options than most 529 Plans. 529 plans are rigid, UGMA & UTMA have wider choices which we will get to later

What are the Cons of starting a UGMA?

The earnings may trigger a tax liability each year.

The deposits are irrevocable. not able to be recovered, regained, or remedied.

Withdrawals may only be made if they benefit your child so if you need the money immediately it might be an issue.

Your child has complete rights to the account upon the stated age (usually between 18-25) so if they make bad decisions with it once handed the account, it’s nothing you can do

Once again, I am not a tax professional or investment advisor please consult experts further on this. Ok, let’s get into the stuff I’m more knowledgeable in the investing side of things. We will use the last model I created on the last newsletter for buying Stocks mixed in with the current model of UGMA

Before we go any further please share, hit the like button, also consider donating towards this newsletter so that I may continue putting out free content of value being that this took time for me to create

BROKERAGE SELECTION

When it comes to investing for yourself & children, the very first thing you need to buy stock or index funds, is to select an online brokerage account. This is the place or platform you use to buy stocks, bonds or other assets. Think of it as a marketplace similar to buying and selling of fruit, Its so many platforms out there to choose from but my personal favorites are TD Ameritrade along with E*TRADE but its others like Vanguard, Fidelity, Webull and Robinhood to name a few that people use. I won’t disparage any platforms but let’s just say that you want to make sure the platform you select is legit, do your research and make sure the platform has a excellent track record and customer service. After all this is the place you will be storing your cash and assets. Ameritrade is the most used platform in my rotation

ACCOUNT SELECTION

This part is where you select your account, and it's what you prefer. Most people select an individual brokerage account to buy stocks, and assets but depending on your age and your goals others such as IRA (Individual Retirement Accounts) or a Roth IRA account are available. There will be questions such as your occupation, margin account or cash account, funding and more but that’s all personal choice for you. What I can say, unless you’re a professional I would not use margin, it’s basically credit for trading or buying stocks and that can get you in deep trouble when the broker does a Margin call, which I’ll allow you to Google that term (Margin Call) now that you have that out the way for yourself you can select your account for your child, the UGMA more than likely will be the choice. Fill in all the requested information

STOCK SELECTION

Once you've set up and funded you or your child’s account, it's time to pick your stocks. A good place to start is by researching companies you already know as a consumer such as Nike, Apple, Microsoft or Google as examples. When looking to invest, take a look at the company's annual report, and management's annual letter to shareholders. These letters give you insight into the future

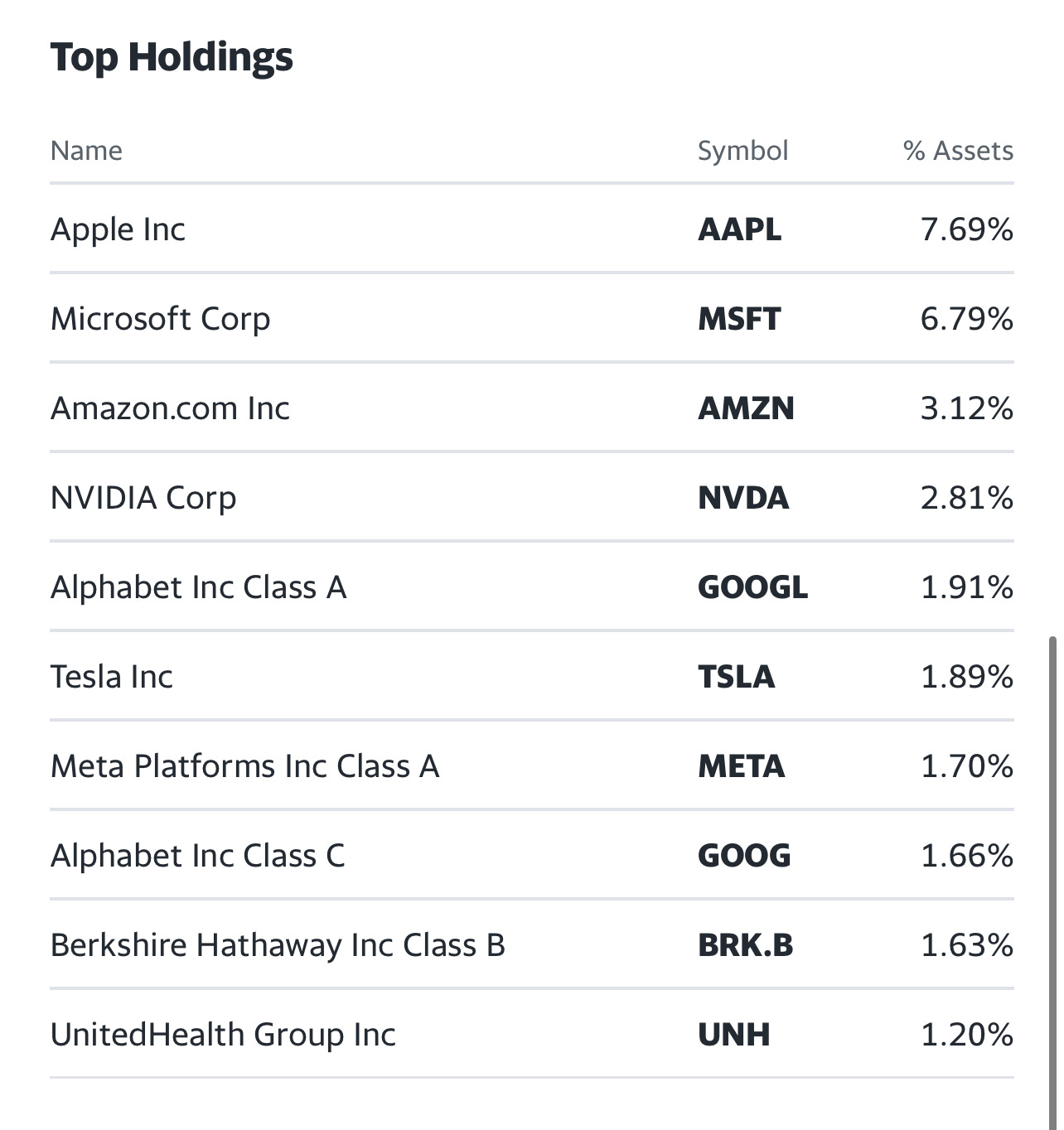

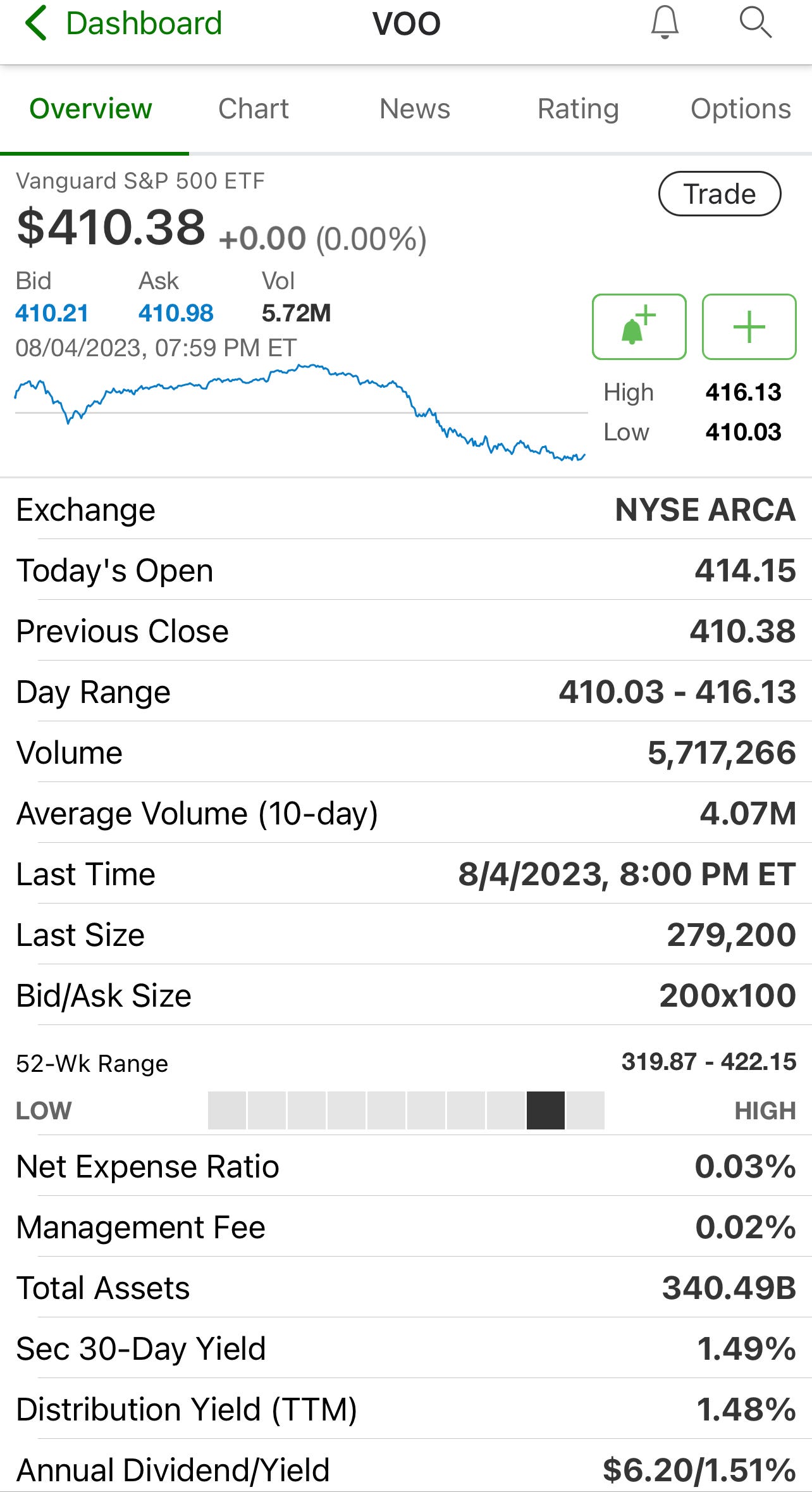

If you’re investing for your child, Index Funds are the most easiest route, it gives you a broad overview and range of everything such as VOO

It’s top holdings are below meaning if it’s a pie, it’s 100 slices, and Apple has 7.69% of the 100 slices

Not every brokerage will offer VOO but it’s pretty much a total stock market selection of the entire Stock Market

RESEARCH TOOL SELECTION

After stock selection, most of the info and tools you need to evaluate the business will be on your broker’s website, such as SEC filings, conference transcripts, quarterly earnings statements and recent news but let’s talk research tools. My personal favorites, and of course I’m biased, so take this with a grain of salt. I like Yahoo Finance, along with CNBC (Apps) because they’re both easy to use, along with the In Depth information they both offer. It’s very important to have tools to go with your stock selection if you want to be successful

DECIDING HOW MANY STOCKS TO BUY

You can start buying stocks with any amount based on how much you can afford. There is no magic number you need to buy based on anything. You can buy a few shares until you have mastered the art of Stock Buying/Trading. Never feel pressured to buy a certain number of shares to fill your entire portfolio position in a stock all at once. Meaning don’t think you have to buy 100 Apple shares, all at once it’s best to diversify your portfolio.

If you’re investing for your child, the best choice is going to be index funds, with low cost maintenance fees to manage it such as VOO but if you’re looking for more in-depth information, scroll to the bottom, it will cost you a small amount or subscription to help towards the cost and time of the information it took to make this content

CHOOSING YOUR ORDER TYPE

There are two order types that you mostly will use for buying stocks, Indexes or others market orders and limit orders.

With a market order, you’re indicating that you’ll buy or sell the stock at the best available current market price.

Never place market order “after hours,” when the markets have closed for the day, because you don’t know what the price will be when you wake up for the day and the market has opened. For example, let’s say you set a market order for Apple, at $100 you could wake and Apple has went up $100 to $200 now you may be overpaying for what you originally wanted. So wait to buy when the market is open between the hours of 9:30am -4Pm (Eastern Standard Time)

A limit order gives you more control over the price of the stock you’re attempting to buy. If XYZ stock is trading at $10 a share and you feel $7 is better or a better value of the stock, your limit order tells your broker to execute your order only when the ask price drops to the $7 level you wanted. So it’s a limit for the price you pay. A “good for day” (GFD) order will expire at the end of the trading day — even if the order has not been fully filled. A “good till canceled” (GTC) order remains till the order expires; that’s anywhere from 60 to 120 days more than likely but don’t quote me on that, every broker is different than the last

Hopefully this beginners guide to investing for your child was helpful to you and if their are any ways I can better assist you let me know. If you’re unfamiliar with my experience I am a very seasoned veteran in buying and selling of stocks along with trading in options. If you’re someone who can benefit from more guidance in investing as a beginner or expert I highly suggest you check out my platform by tapping this link to Patreon also in addition to this I also have a YouTube channel called The Monk Investor where I create documentary style visual content to help you understand investing along with the world as a whole. If you’re a visual learner, I highly suggest you watch this video Stock Market For Beginners and subscribe

*****************

Disclaimer: The Monk Investor Newsletter uses information from various sources believed to be reliable, but the accuracy cannot be 100% guaranteed. So please treat information contained in this publication as not individual investment advice for your personal financial situation. You are advised to discuss your investment options with your financial adviser. Consult your financial adviser to understand if any or all investment is suitable for your specific needs. I may, from time to time, have positions in the securities covered in the articles on this website. This is not a recommendation to buy or sell stocks it’s more so for entertainment and research purposes. Thank you